The Problem With German Banks

Lies. Misfortune. Mishap.

Deutsche Bank and Commerzbank headquarters in Frankfurt, Germany

In the months leading up to the 2007 and 2008 financial crisis, Deutsche Bank sold “junk” bonds to investors; promoting them as A-grade.

In 2013, German banks cheated on the European Central Bank’s stress tests, a Bundesbank study later revealed.

In June 2020, Wirecard reported a missing hole of $2 billion in its balance sheet. Wirecard’s CEO was arrested.

German banks are struggling to keep up with rising costs, low profitability, and strict requirements imposed by the European Central Bank (ECB). In addition, the corrupt inner workings of the German banking system has emerged as a top priority for politicians, investors, and regulators to tackle.

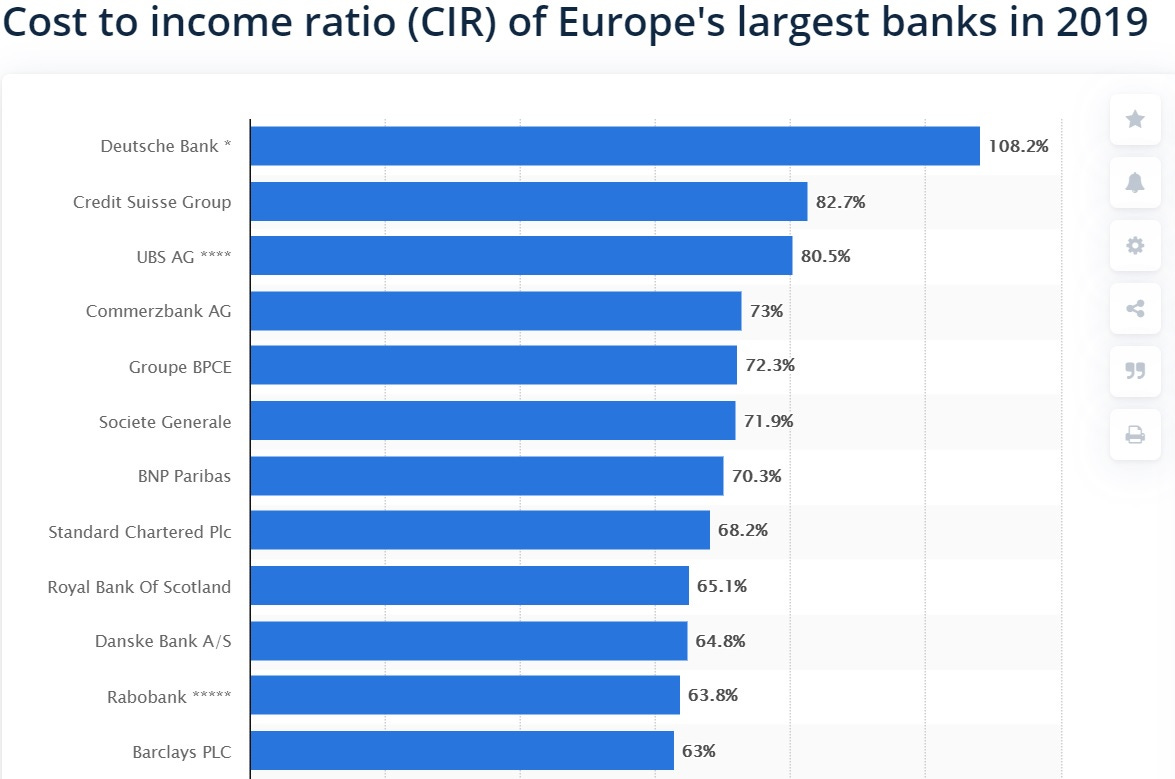

Rising Costs and Low Profitability

Source: Statista

One problem German banks struggle with is Cost to income ratio.

Cost to income ratio (CIR) determines the profitability of banks by comparing the cost of running operations to a bank’s operating income.

A lower CIR means that the bank is running more profitably, while a higher CRI indicates that the bank’s operating expenses are too high.

As of 2019, the cost to income ratio for German banks on average sits around 85%; much higher than its European counterparts which hover around 63%.

Low profitability has been highlighted by the ECB as a key risk to financial stability.

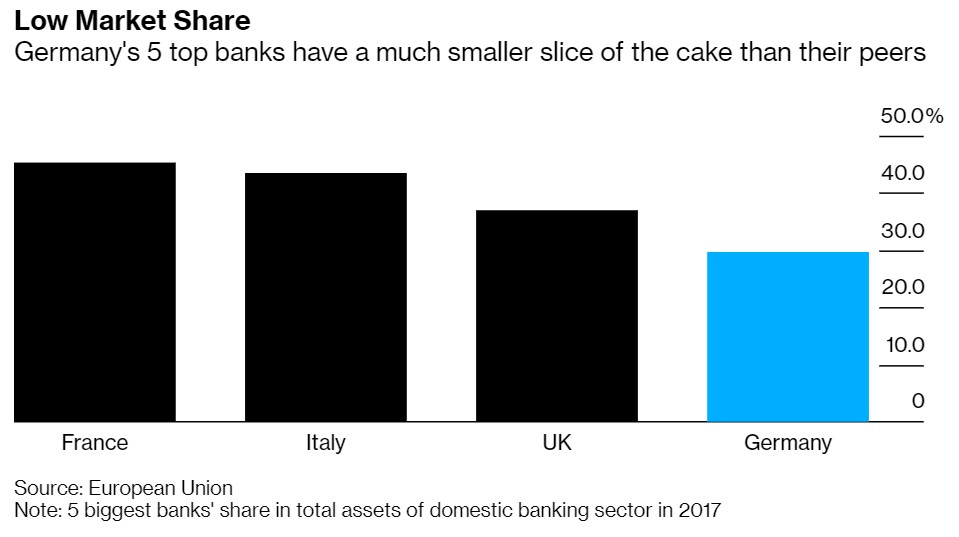

Strict Rules

Another setback is that German banks struggle with strict rules imposed on them by the ECB.

Source: Bloomberg

The ECB imposes higher requirements on German banks more so than other European banks.

This limits shareholder return, and German banks already make up less percent of the overall market cap than other European countries.

Source: Bloomberg

However, as recent as March 2020, German regulators cut capital requirements in order to boost bank lending.

“The cut… should give banks a capital boost of around 5 billion euros ($5.48 billion).”

“The currently weak revenue situation is a big challenge for the German banking sector,” the German finance minister said in May 2019, “It’s important that banks review their business models and adapt them if necessary to support a positive economic development in Germany in the long run.”

Deutsche Bank. Downhill Since

During the 2007 and 2008 financial crisis, Deutsche Bank’s stock price plummeted nearly 84% to just $25 per share-down from an all-time high of $159 per share two years earlier.

Source: Google Finance

Since then, Deutsche Bank hasn’t recovered, and its stock price still wavers around $10 per share. Amid numerous scandals and controversies, Deutsche Bank’s history is gloomy and despised.

It seems to never learn from its past mistakes, and scandal after scandal, Deutsche Bank diminishes its trust with investors and German citizens.

In 2017, Deutsche Bank agreed to a $7.2 billion settlement with the U.S Department of Justice for selling “crap” and “junk” bonds and misleading investors in the months leading up to the 2008 financial crisis.

A United States Senate investigation into the 2007 and 2008 financial collapse revealed that Deutsche Bank’s top global Collateralized Debt Obligation (CDO) trader, Greg Lippmann, warned his colleagues and clients of the poor quality of certain securities and assets, saying that they were “crap” and “pigs,” and anticipated those assets and securities to “lose value”, even though many had AAA ratings. Many of these poor quality securities are now “virtually worthless.”

Regardless, Deutsche Bank sold about $700 million in assets, without disclosing the extremely negative views it’s top CDO had of roughly a third of assets held by Deutsche Bank, which had lost over $19 million in value since they were purchased.

“Within months of being issued, the… securities lost value; by November 2007, they began undergoing credit rating downgrades; and by July 2008, they became nearly worthless.”

In an email regarding certain assets held by Deutsche Bank, Lippmann wrote:

“[H]alf of these are crap and rest are ok…”

The investigation continues, stating:

“Deutsche Bank’s senior management disagreed with [Lippmann’s] negative views, and used the bank’s own funds to make large proprietary investments in mortgage related securities…”

The investments in mortgage-related securities made by Deutsche Bank had a face value of $128 billion, and a market value of $25 billion.

Despite its optimistic view of the housing market, Deutsche Bank allowed Lippmann to open a large short position Residential Mortgage-Backed Security (RMBS) market, which from 2005 to 2007 totaled $5 billion. From 2007 to 2008, Deutsche Bank cashed in on the position which totaled a net profit of $1.5 billion.

“Lippmann claims [this] is more money on a single position than any other trade [he] had ever made for Deutsche Bank in its history.”

Although Deutsche Bank gained a monumental amount of money from Lippmann’s short position, Deutsche Bank altogether lost nearly $4.5 billion from its mortgage-related investments.

Since 2012, Deutsche Bank has paid more than €12 billion (roughly $13.5 million USD) for legal action taken against them.

ECB Stress Test: Manipulated

Frankfurt, Germany

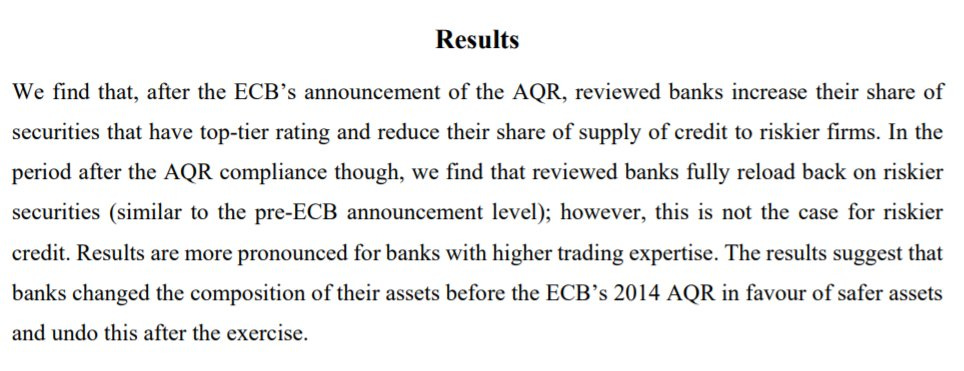

When the European Central Bank (ECB) conducted an asset quality review (AQR) in 2013, it attracted a lot of attention from financial experts and researchers.

Most notably, a group of financial experts from Deutsche Bundesbank, Imperial College London, and the US Federal Deposit Insurance Corporation reviewed the ECB’s AQR data and analyzed whether or not those banks deliberately altered their assets’ risk composition before the reporting date.

In the Bundesbank study, the researchers stated:

“We use the European Central Bank (ECB)’s 2014 asset quality review (AQR)… [to] analyse whether banks dress up for the regulator by changing the risk composition of their portfolio before the AQR’s point-in-time reporting date (31st December 2013).”

The researchers evaluated 130 banks that have €22 trillion ($24 trillion) in assets, including 25 German banks, before and after the review was conducted in 2014.

What they found was evidence of banks lying on the test by downsizing riskier assets before being reviewed by the ECB in order to put the banking industry in a better light.

Shortly after the review would be conducted, banks would sell safer assets and reinvest into assets with higher risk factors.

“…after the asset quality review is concluded (July 2014), banks will liquidate these safer assets and will invest back in assets with a relatively higher risk.”

The report further stated:

“There have been several instances of banks that have passed the stress tests and then failed within a short period of time thereafter… supervisors are aware of the risk-masking incentives by banks.”

Wirecard’s Missing $2 billion

Wirecard’s CEO, Markus Braun, was arrested shortly after the company reported $2 billion missing from its balance sheet

Once the fintech star of Germany, Wirecard is now among the rubble of companies riddled with shady operations.

Its stock plunged amid news in June that $2 billion had seemingly disappeared from the company’s balance sheet.

Since June, Wirecard’s stock has lost 97% of its value. It dropped even further after the company reported that the $2 billion probably didn’t even exist.

“[There is] a prevailing likelihood that the bank trust account balances in the amount of €1.9 billion ($2.1 billion) do not exist.” -Wirecard

The payment processing company touched base with IKEA, FedEx, and Aldi, but data now suggests that the company used third parties to generate business in order to make it appear larger than it actually was.

About two years earlier, a whistleblower told officials that the local Wirecard finance team in Singapore had created false invoices and contracts in order to seemingly boost revenue. This led the Singapore police to launch an investigation into Wirecard roughly one year after it was first reported.

Wirecard withdrew its financial results for 2019 and the first quarter of 2020.

A small law firm in the Philippines, which was responsible for overseeing Wirecard’s cash, told Wirecard’s main auditor that the $2 billion had been moved to two new banks, BDO Unibank Inc. and Bank of the Philippine Islands, both in the Philippines. Electronic scans of bank confirmation letters were later sent to Wirecard. However, those two banks later denied ever having held any money on behalf of Wirecard, and the bank confirmation letters were proven to be a fraud.

Amid this news, Wirecard’s CEO Markus Braun was arrested on suspicion of inflating the company’s balance sheet and sales in order to make it more attractive to investors and customers.

Wirecard, once worth $14 billion, is now valued at less than $2 billion.